Going into the earnings season, credit card transaction processing companies like Visa (V) and MasterCard (MA) have been hit pretty hard due to adverse impacts of the recently approved financial reform regulation which limits the interchange fees they can charge banks and merchants for card transactions. However the actual regulation in the financial reform bill was scaled back to only cover debit card network fees, which impacts the banks more than it would Visa (V) or it’s card processing competitor MasterCard (MA). Following the public release of the financial reform bill, Visa and MasterCard stock prices dropped nearly 20% from recent highs within just a couple of weeks. While they have recovered somewhat along with the broader market in improving and more certain market conditions I think the stocks have much more upside going into earnings. In fact a fairly risk free trade, albeit with a bit of initial up-front capital, is to buy the stock before earnings (see dates below) and buy put options to cover any short-term down side risk.

In particular I think the international growth potential of Visa an MasterCard will offset any adverse impacts of the domestic financial regulation costs. International revenues and margins from foreign operations are already starting to account for a significant portion of these companies revenues, particularly from a still booming Asian economy. Further, with the threat of another Euro-American economic slowdown for later this year, V and MA both offer better than average down side protection as shown in the past few years as the stock prices reached new highs. Thus the longer term outlook of both these companies looks strong.

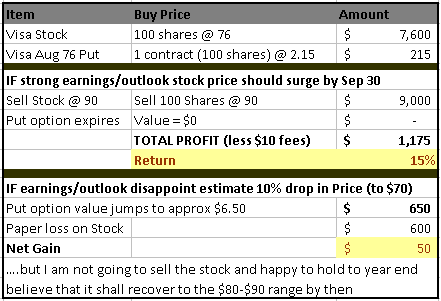

and MasterCard (MA) trade") The table here shows the relatively simple trade I am going to be putting on for Visa (since it reports earlier) using the stock and a single put option contract (prices at COB 7/26). As you can see the trade is to buy 100 stocks and a single August $76 put option contract (one contract equals 100 shares). If the earnings and outlook are strong, the stock price should rise to near $90 and I make $1,175 (15%) within a couple of months as analysts reassess the stock’s growth prospects. However, if there is a negative surprise and earnings miss and/or the outlook is below expectations the stock will fall soon afterwards, and the put option can be sold for a profit (200% return). While I will have a paper loss on the stock should it drop below $76, I will keep holding until it recovers as I believe the longer term outlook is still very strong.

The table here shows the relatively simple trade I am going to be putting on for Visa (since it reports earlier) using the stock and a single put option contract (prices at COB 7/26). As you can see the trade is to buy 100 stocks and a single August $76 put option contract (one contract equals 100 shares). If the earnings and outlook are strong, the stock price should rise to near $90 and I make $1,175 (15%) within a couple of months as analysts reassess the stock’s growth prospects. However, if there is a negative surprise and earnings miss and/or the outlook is below expectations the stock will fall soon afterwards, and the put option can be sold for a profit (200% return). While I will have a paper loss on the stock should it drop below $76, I will keep holding until it recovers as I believe the longer term outlook is still very strong.

{kind=link}

Visa Inc. (NYSE: V) is scheduled to report its Q3 2010 results after the market closes on July 28, 2010. Analysts’ estimates for Q3 2010 range from a low of $0.87 to a high of $0.98, compared to a consensus estimate of $0.93. MasterCard (NYSE: MA) is schedule to report on August 3rd 2010. Given Visa reports first I am going to execute the trade above for V first. If it works, then the same trade for MasterCard (MA) is next. I will post the results of my trade on this post after it is made.

Results from Yahoo.com

Visa Inc. on Wednesday said its third-quarter profit slipped 2 percent, hurt by a sharp drop in investment income, but it posted increased operating income and maintained a strong forecast for its fiscal year. The San Francisco company posted net income of $716 million, or 97 cents per share, for the period ended June 30. That compared with net income of $729 million, or 97 cents per share, in the year-earlier quarter.

Revenue rose 23 percent to $2.03 billion from $1.65 billion last year. The results topped Wall Street expectations for profit of 93 cents per share on revenue of $1.97 billion.

Chairman and CEO Joseph Saunders said in a statement that Visa saw improvements in global cross-border transactions and payments volume. Cross-border volume rose 17 percent for the quarter, while total processed transactions gained 14 percent, to 11.7 billion.

The company, which says about 70 percent of all the transactions it processes now involve either debit or prepaid cards, said debit card use in the U.S. rose 19 percent to $352 billion during the quarter. Credit card transactions, which fell in recent quarters, rebounded slightly, gaining 2.2 percent to $214 billion.

In the rest of the world, debit use shot up 24 percent to $383 billion, while credit volume jumped 19 percent to $320 billion.

Visa said it’s too early to tell what impact it will feel from limits to the fees charged to merchants for processing debit card payments that were written into the financial overhaul law signed by President Barack Obama last week.

“It goes without saying, the United States debit market will undergo changes following implementation of the Wall Street reform and consumer protection act next year,” Saunders said.

He added that the new rules will not stem the global shift from cash and checks to plastic.

“I really don’t believe in my heart of hearts that it is going to stop electronic payments from growing in the United States,” Saunders said during a conference call to discuss the third-quarter results. “What that means, what form that takes, how that changes our business model, I’m just not able to specify that at this particular point in time. But you should take some confidence in knowing that we are paying attention. I’m not just sitting on our hands waiting for something to happen.”

Andy Miedler, senior technology analyst at Edward Jones, said the uncertainty regarding the regulatory reforms has weighed on Visa’s stock, but the earnings results showed the quarter was “business as usual for Visa.”

He said he expects the final rules regarding the debit card fees, which will be written by the Federal Reserve, will have only a modest earnings impact.

“The Fed has been a fair body looking at interchange in the past,” he said, using an industry term for those fees. “We have hopes for the same going forward.”

Visa is now focusing on its acquisition of CyberSource Corp., which closed last week. The purchase seeks to tap the growing global market for online payments and make use of CyberSource’s fraud prevention technology. CyberSource has a hand in processing about 25 percent of all U.S. e-commerce payments.

The company said it continues to expect revenue growth of 11 to 15 percent in its fiscal year, and earnings per share growth of 20 percent or higher.

That implies full fiscal year revenue of between $7.67 billion to $7.95 billion, and earnings per share of at least $3.72.

Wall Street has forecast, on average, annual revenue of $7.97 billion and earnings per share of $3.90.

Visa’s shares edged up 2 cents, to $75.20 in aftermarket electronic trading, from their close in the regular session at $75.18.

Investors looking for a rally after V’s earnings announcement could consider buying the January 2012 65 LEAPS calls for $19.50 per contract or better. These options could take advantage of longer-term volatility and will not be subject to time decay during the near term. The premium paid on this long call trade also represents the maximum risk. If the stock does not rally higher than the strike price by January 2012 options expiration, the investor loses 100% of the debit.

If the stock rallies at least 11% during the long term and is trading higher than $84.50 at expiration, the investor could theoretically make unlimited profits to the upside. If the stock is trading between the strike price and the breakeven price, the investor will take back some, but not all, of the debit on the options.

Visa says 70 percent of all payment transactions in the U.S. are now debit or prepaid. Debit cards passed credit cards in popularity a few years ago, particularly for smaller purchases. So they make take more of a hit than you indicate. But it will be interesting to hear what they say about ” the new swipe fee limits charged to merchants when their customers pay with debit cards.” UBS analyst Jason Kupferberg said the swipe fee limitations represented “an unexpected turn for the worse,” but added that traders have sent the shares down too low in response. He expects the new regulations “will ultimately prove to be manageable, rather than catastrophic.”

Visa is one of my favorite stocks going forward…this might not have anything to do with anything, but if you noticed all the advertisements for Visa in the World Cup, they were all over the place. When Visa had a ton of advertisements for the Winter olympics the stock seemed to perform well that in those months and therafter… I thought about this when I was watching a lot of the World Cup this year. Again, just a random observation and probably doesn’t have to do with anything.

Hey – if you find a trend that works and power to you. What you said doesn’t sound that far fetched. Also it is just another sign that the international market is where the growth is and that is why Visa is advertising so heavily

While I expect this trade will work out for you, it seems that you are obscuring the risk that actually exists. It is possible, if unlikely given recent volatility, that there will not be enough price movement to justify selling either the stocks or the options before the options expire, followed by an extended stock decline after that point.

I’ve often wondered how well option prices capture expected volatility — which, of course, leads to the question of how well expected volatility matches reality. This is what has kept me out of the option game. I’ve made (or considered) other volatility anticipated trades and then watched the stock price stagnate for months. I think it is easy to fall into the trap of thinking that a given stock must either rise or fall, but that obviously isn’t always the case.

You are correct, I do need volatility for the put option to work. But I am using it more as downside protection instead of trading the expected volatility. However, I still think the stock is a good longer term story and am happy to hold for 6 or more months.